In a 2021 report titled Payments are Eating the World, J.P. Morgan stated that the next decade will see revolutionary and foundational changes within the payments industry. But how could blockchain applications, specifically, help this essential and all-encompassing field?

Blockchain For Payments: The Continued Disruption Of Payments

Payments can mean all sorts of different things to different people. If you run a small business, it might mean people paying for your product in-store with a card (also known as business to consumer or B2C). If you sell a product or service to another business, you might think of it as sending an invoice to them and receiving money (also known as business to business or B2B payments). These are just a couple of practical examples, but of course, the list goes on.

It’s a huge, complex, and fast-moving industry and the term “payments” can be used to cover any process where money changes hands. In this article, we’ll take a look at how blockchain already impacts the payments industry, as well as how it could evolve in the future in the face of ever-changing regulations and technologies.

A standard such as ISO 20022 now mean that there’s a new global protocol for payments between financial institutions. Beyond the new regulations, technologies like AI, quantum computing, and blockchain have forced the payments industry to move faster than ever, with major new developments being made every year.

“It’s no surprise that payments is a business open to great disruption by fintech companies. Traditional payment systems were built long ago and customer expectations have evolved quickly and dramatically along with the technological advancements we’ve experienced in our personal lives.”

— J.P. Morgan

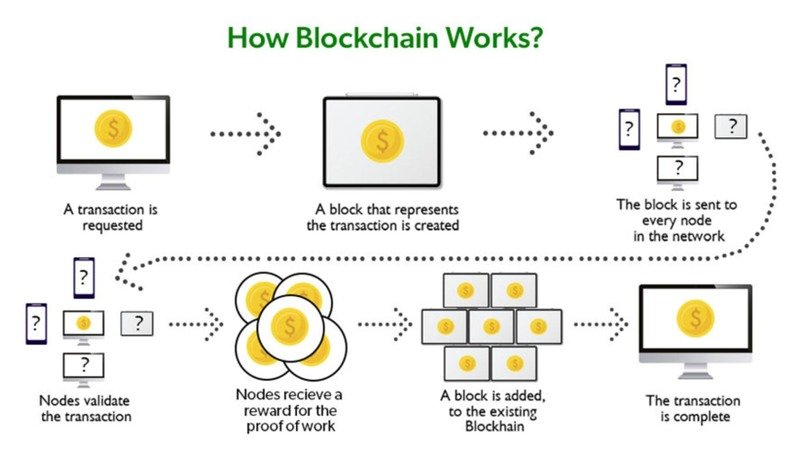

J.P. Morgan’s 29 page report mentions blockchain 15 times and suggests that its acceptance by businesses and institutions is only going to increase. It seems this distributed ledger technology, used to record transactions across a network and ensure transparency and immutability, is here to stay.

But the broader payments system is being disrupted even today by companies like Revolut and Stripe. How might it evolve into the future as blockchain applications become increasingly popular?

Blockchain For Payments Beyond Crypto

The core idea behind blockchain (although surprisingly, not the term itself) was famously created by Satoshi Nakamoto in the Bitcoin Whitepaper. It might have originally been developed as a platform for cryptocurrencies to run on, but the underlying technology has a plethora of applications far beyond that. But unfortunately, in the intervening years, blockchain’s association with crypto has probably done more harm than good to its reputation!

Blockchain payment protocols have big advantages over other payment methods, including enhanced security, increased efficiency, and reduced costs. The decentralized and cryptographic nature of blockchain makes it resistant to fraud and its peer-to-peer nature streamlines transactions and eliminates reliance on third-parties that we see in many processes today.

“The blockchain is the financial challenge of our time. It is going to change the way that our financial world operates.”

— Blythe Masters, financial services entrepreneur & former J.P. Morgan executive

Its applications span various industries, from e-invoicing to supply chain finance and microtransactions. Here’s a deeper look at where it might help some of these in the not-too-distant future.

Accounting

In our previous overview of how blockchain is revolutionizing accounting, we looked beyond payments directly and at how blockchain can be and is being used to enhance the recording of financial information. By providing a decentralized ledger that records transactions in a secure manner, blockchain reduces the likelihood of fraud and helps ensure that financial records are accurate and tamperproof.

Wider adoption of blockchain could lead to a reduction in the time and cost associated with audits and financial reporting. It could also help automate many of the routine tasks that accountants perform, such as reconciliations and processing transactions, through the use of one of blockchain’s features: smart contracts.

These contracts execute the pre-agreed terms automatically when certain conditions are met, further streamlining accounting processes and reducing the potential for human error.

Another innovative practice, triple-entry bookkeeping, allows both parties to view and verify transactions and cuts out the need for an audit trail or reconciliation with an intermediary.

Using blockchain to record transactions opens up a world of possibilities, everything from real-time financial reporting to improving the quality and reliability of information. This improved visibility into a company’s finances would be a game changer for the accounting industry and offer a more dynamic and accurate picture of a business’s financial health.

Supply Chain Finance

The supply chain finance (SCF) industry might not be as well known as accounting but its certainly no less important, particularly for those living in developing nations. SCF is a set of processes that link various parties in a transaction — buyer, seller, and financing institution — to lower financing costs and improve business efficiency. It’s often used to provide short-term credit to a buyer or seller and enhance liquidity whilst reducing the risk for both parties.

Demand for SCF is growing quickly. It’s estimated that global SCF transaction volumes grew 21% in 2023 to $2.1 trillion and the growth was even greater in Africa and Asia at 39% and 28% respectively. The practice itself goes back thousands of years but as it’s evolved, so have the problems associated with it. Large financial institutions are often reluctant to lend to emerging markets — the primary reason being a lack of trust between the parties involved. Blockchain might have its own issues, but its ability to verify transaction history and payment reliability offers a great solution to this particular problem.

Barclays issued the first-ever blockchain-based letter of credit in 2016 and hailed blockchain as “a technology that promises to transform trade finance over the coming decade.” The technology has, arguably, undelivered on that promise, although how much of this is down to the technology itself vs. the inertia of the institutions involved is unclear. Work to grow the role of blockchain-based protocols in SCF is still ongoing.

A 2020 article by Harvard Business Review studied how seven major US companies, including IBM and Mastercard, are using blockchain to improve their supply chain and SCF processes. They found that blockchain applications can be useful to small and large organisations alike, and that a large part of their appeal to some is that they require the companies involved to share only limited data.

“When inventory, information, and financial flows are shared among firms through a blockchain, significant gains in supply chain financing, contracting, and doing business internationally are possible.”

— Harvard Business Review

The study also points out that while adopting blockchain can enhance efficiency and security, successfully implementing it requires careful planning and shouldn’t be undertaken lightly. With the right approach however, the rewards can be substantial.

Fundraising

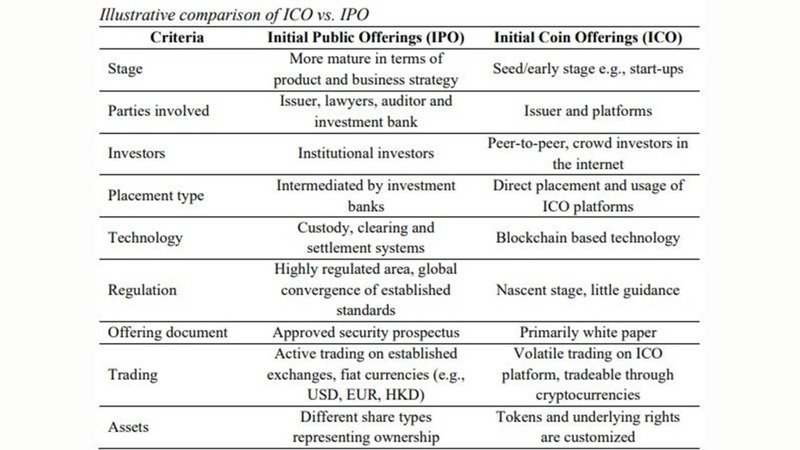

One interesting area of study at the moment is the use of initial coin offerings (ICOs) to raise funding for projects. But, perhaps like blockchain itself, this new method of funding has gained an unfortunate reputation over the last 6 years. This is largely thanks to the fraudulent projects that got involved with it from 2017 to 2018. Unlike those projects however, ICOs themselves do have genuine use cases.

An IPO is when, rather than only private entities being able to invest in a company, the public get the chance to invest in it too. An ICO is somewhat similar but in the crypto world.

With ICOs, rather than raising capital from angel investors or venture capitalists, the creator of the project can raise funds in a peer-to-peer manner through selling the coin directly to other people. This cuts out the need for large investment institutions and allows everyone to invest in it (at their own risk of course!), no matter how small their contribution.

Perhaps the main issue with this at the moment is the reputational hangover from previous ICO projects which were seen as get-rich-quick schemes by many. But if this reputation can be shaken off and the regulatory issues around ICOs, and the broader Web3 ecosystem, can be sorted out, then perhaps blockchain-based ICOs will become Web3’s answer to today’s crowdfunding platforms.

Blockchain Within Payments

So we’ve seen that blockchain will likely have a large part to play in the future of the financial industry as a whole, but what are some specific use cases for blockchain within payments directly?

E-Invoicing

Combining blockchain and invoicing allows companies to create immutable and transparent records of transactions, while also helping to ensure their authenticity and traceability. Using a public blockchain for recording invoices makes transactions easy to monitor and provides a simple audit trail for anyone to follow to verify the reliability of the payor.

Many of the traditional problems with today’s invoicing, such as human error and miscommunication, could be avoided. Companies like Populous World tried to do this in the late 2010s, but were perhaps a bit ahead of their time.

In February 2023, mintBlue, a blockchain as a service (BaaS) platform, announced an integration with the Dutch Chamber of Commerce and Visma | Yuki, an accounting software company with 1.7 million customers. The agreement allows for the automatic verification of the sender/receiver when processing an invoice, improving efficiency and lowering the risk of fraud.

“The new integration allows us to indicate with higher assurance that an invoice is secure. In a time of regulation changes for privacy, security and ownership, we were very impressed with how easy it was to embrace innovation and advance our e-invoicing technology through mintBlue. Immutable storage and automation of identity-verified invoices is critical to fraud reduction and the future of e-invoicing. We are very excited about this solution and look forward to the growth of the ecosystem.”

— Jeroen van Haasteren, CTO of Visma | Yuki

mintBlue’s Software Development Kit (SDK) means that payment processors can publish their invoices on the BSV blockchain and eliminate the need for reliance on auditors and third-parties to verify the transactions.

It’s initiatives like this that showcase a prime example of how blockchain can help companies process payments and deal with invoices. Blockchain is no less useful when it comes to identity verification, especially at a time when generative AI, and the ability to easily create fake documents, is improving so quickly.

AML & KYC

Anti-Money Laundering (AML) and Know Your Customer (KYC) checks are essential for many businesses nowadays, especially those in fintech where the regulatory environment moves incredibly fast.

“KYC and AML have well surpassed the boundaries of professional jargon within the banking sector. They’re at the very heart of financial security, and regularity compliance, and are essentially the pillars that support banking’s integrity.”

— Fraud.com

At the moment however, there are issues with these checks. For one, it’s difficult for cross-border banks, which need to comply with regulations across multiple jurisdictions, to keep up. It’s also hard to provide a good user experience whilst ensuring that the procedures are followed correctly.

As is the case with e-invoicing, this could become even more difficult in the future as technologies like generative AI mean that fake documents can be cheaply and easily generated. Companies like OnlyFake claim to use AI to generate realistic photo IDs for just $15. Could this end up creating yet another form of an AI arms race? One in which the creators use AI to make fake documents, and the law enforcement agencies use AI to ascertain whether the documents are fake or not? There must be an easier way.

The configurability of blockchain means that the right people can have access to available customer data whilst also making it traceable and verifiable. The principle behind this is simple: each piece of data recorded on the blockchain is linked to the previous one.

When applied to digital identities, this means that every modification or verification of a user’s ID data is logged. Authorized entities can then access this data to confirm the authenticity of an individual, relying on cryptographic proofs to guarantee the data’s integrity without compromising the individual’s privacy. This helps creates a more secure digital identity ecosystem and ensures the integrity of personal data, thereby enhancing privacy and trust.

Relying on a blockchain to verify an individual’s identity rather than documents also means that fakes and forgeries can’t be used to game the system. If the data can’t be verified on the blockchain, then it shouldn’t be trusted.

Micropayments

Micropayments, small financial transactions often less than a dollar, have become increasingly popular in recent years, especially in the gaming industry. Traditional payment system processing fees can make such small transactions impractical, but blockchain can allow for cost-effective micropayments.

This opens up the possibility for new business models and content monetization strategies such as pay-per-use services. The Brave browser, for example, uses blockchain to allow users to make Bitcoin micropayments to their favourite content creators. And this is just one example of the potential of micropayments to transform online revenue models.

Blockchain also allows players to trace the previous ownership and origins of in-game items. Could we one day see a video game where an item’s value is partly based on its prior owners rather than its aesthetics or practical use?

With blockchain, micropayments could also become a more common payment method on social media platforms. People could pay $0.02 to view a single blog post or video from their favourite content creator rather than a $10/month subscription to view everything, including a whole lot of content they don’t care about. Consumers would only pay for the content they view and it would open up another source of revenue for creators. Apps like Diamond, which runs on the DeSo (Decentralised Social) blockchain, allow users to tip “diamonds” to creators. The money is then taken directly from a user’s wallet and sent to the creator. Each creator also has their own coin with the price fluctuating according to demand for it, which (ideally) increases according to the quality of their content. Yet another incentive for creators to produce high quality content rather than just spam people and hope for engagement.

Diamond has a very similar UI to Twitter/X, but users can tip their favourite creators with diamonds, supporting them if they enjoy their content.

In our next article, we’ll take a deeper look at blockchain in the micropayments industry and cover some of the larger issues with it.

Conclusion

The transformative potential of blockchain within the payments and broader financial industry could be revolutionary. The discourse around blockchain sometimes gets caught up with its association with cryptocurrencies. However, as we’ve seen, its applications extend far beyond that of crypto.

Blockchain platforms are poised to disrupt traditional payment systems, which I believe are becoming increasingly viewed as outdated in the face of modern technologies and their rate of improvement. It might have its issues, but it offers a solution to many of the problems plaguing the payments industry today. Blockchain has been around for about 16 years now and its clear that this technology isn’t just a passing fad. With its unique attributes and broad range of applications, it offers a platform that could play a major role in the payments industry in the coming years.

Read Also: What Is Data Governance In Banking?

Disclaimer: Information provided on AlexaBlockchain is for informational purposes only and not financial advice. Crypto investments, including ICOs, IDOs, presales, and other token offerings, are highly risky. You are responsible for conducting your own research (DYOR) before making any financial commitments. Take professional advice before making any investment. Read complete disclaimer here.